Distributor assessment in route-to-market work has a predictable structure. A framework identifies dimensions - typically four to seven - along which a distributor can be evaluated. Financial Health. Warehouse capacity. Vehicle fleet. Market presence. Team capability. Strategic fit. Each dimension gets a score, the scores roll up into a composite, and the composite produces a verdict: RETAIN, DEVELOP, REPLACE, or EXIT.

The framework is useful. It forces structured assessment instead of gut feel. It makes distributor reviews comparable across territories. It produces defensible verdicts that survive boardroom challenges. The framework is not, however, where the real conversation happens.

The real conversation, in my experience, is almost always about working capital. And most frameworks treat it as one dimension among many, when it's actually the dominant one.

The numbers that tell the story

Consider a specific scenario. The East Java territory is being re-appointed after the incumbent distributor's contract expired. The SP builds out the ideal candidate profile - a new distributor positioned as "Offensive Growth", targeting a significant share expansion over three years. The investment requirement, calculated through the platform's distributor P&L model:

Vehicle fleet (eight motorcycles for DSR routes): IDR 240 million. Warehouse fit-out (800 square metres, racking, climate control): IDR 180 million. DSR recruitment and onboarding (eight DSRs, three months of ramp-up): IDR 96 million. Working capital (inventory float, receivables cycle, transition buffer): IDR 1.84 billion.

Total investment: IDR 2.36 billion.

The working capital line is 78% of the total. Vehicles, warehouses, and DSRs combined are 22%.

This isn't unusual. In distributor after distributor, across categories, the pattern repeats. Working capital is the dominant constraint on viability, and most of the other dimensions are operational details around it. A distributor with a smaller warehouse can make it work. A distributor with fewer vehicles can route-optimise. A distributor short on working capital cannot operate at all.

Why working capital is structurally dominant

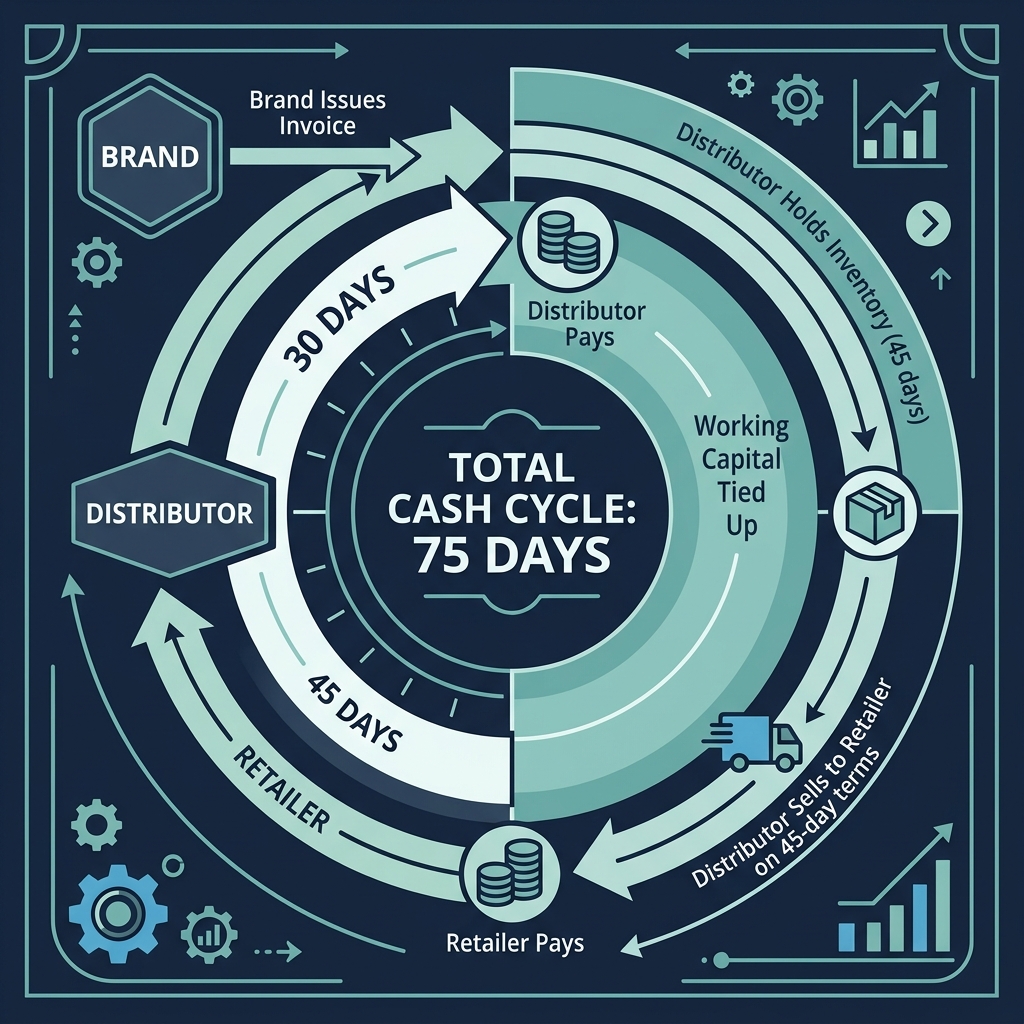

The economics are straightforward. A distributor holds inventory - typically 45 to 60 days of stock, depending on the category's replenishment cycle and the distance to the manufacturer. They extend credit to retailers - typically 30 to 45 days for modern trade, longer for some traditional trade segments. Their own payable terms to the manufacturer are typically 30 days. The cash cycle - the gap between paying for inventory and receiving payment from retailers - is usually 60 to 90 days.

Multiply that cycle by the monthly volume, and you get working capital tied up in the business. A distributor handling IDR 1 billion of monthly volume with a 75-day cash cycle needs roughly IDR 2.5 billion of working capital just to keep operating. That's IDR 2.5 billion sitting in inventory and receivables at any given time, not available for investment or distribution.

Increase the volume by 30% - the growth ambition in a typical Offensive Growth scenario - and working capital needs to scale proportionally. If the distributor can't fund the working capital expansion, the growth can't happen, no matter how capable their team or how good their warehouse. The constraint is cash, not capability.

The lever nobody pulls first

Here's where the conversation gets interesting. Working capital isn't fixed. The biggest lever is the credit terms the brand extends to the distributor. If the brand's payable terms are 30 days, the distributor's working capital requirement is higher. If the brand extends terms to 60 days, the distributor's working capital requirement drops substantially.

In the East Java scenario, extending brand credit terms from 30 days to 60 days reduces the distributor's net working capital requirement by IDR 420 million - a 23% reduction on a IDR 1.84 billion base. That's equivalent to finding an extra IDR 420 million in the distributor's balance sheet, without either party actually putting in more cash. The lever is a term sheet change, not a capital injection.

Most brands don't think about distributor credit terms this way. They think about DSO (days sales outstanding) as a finance metric to minimise - shorter payment terms mean better cash flow. That's true for the brand in isolation. It's wrong for the brand-plus-distributor system. Squeezing the distributor's payment terms by 30 days transfers IDR 420 million of working capital burden from the brand to the distributor. If the distributor can't fund it, the growth plan fails and the brand loses the territory. The brand has optimised its DSO at the cost of the commercial objective.

The best-in-class distributor relationships in Southeast Asia - the ones where distributors actually grow at brand-target rates - have credit terms structured as a lever, not a fixed input. Growth scenarios get longer credit terms to fund the working capital expansion. Mature territories get shorter terms as the distributor stabilises. The brand treats credit terms as a co-investment tool, not a finance metric.

Reframing the distributor P&L

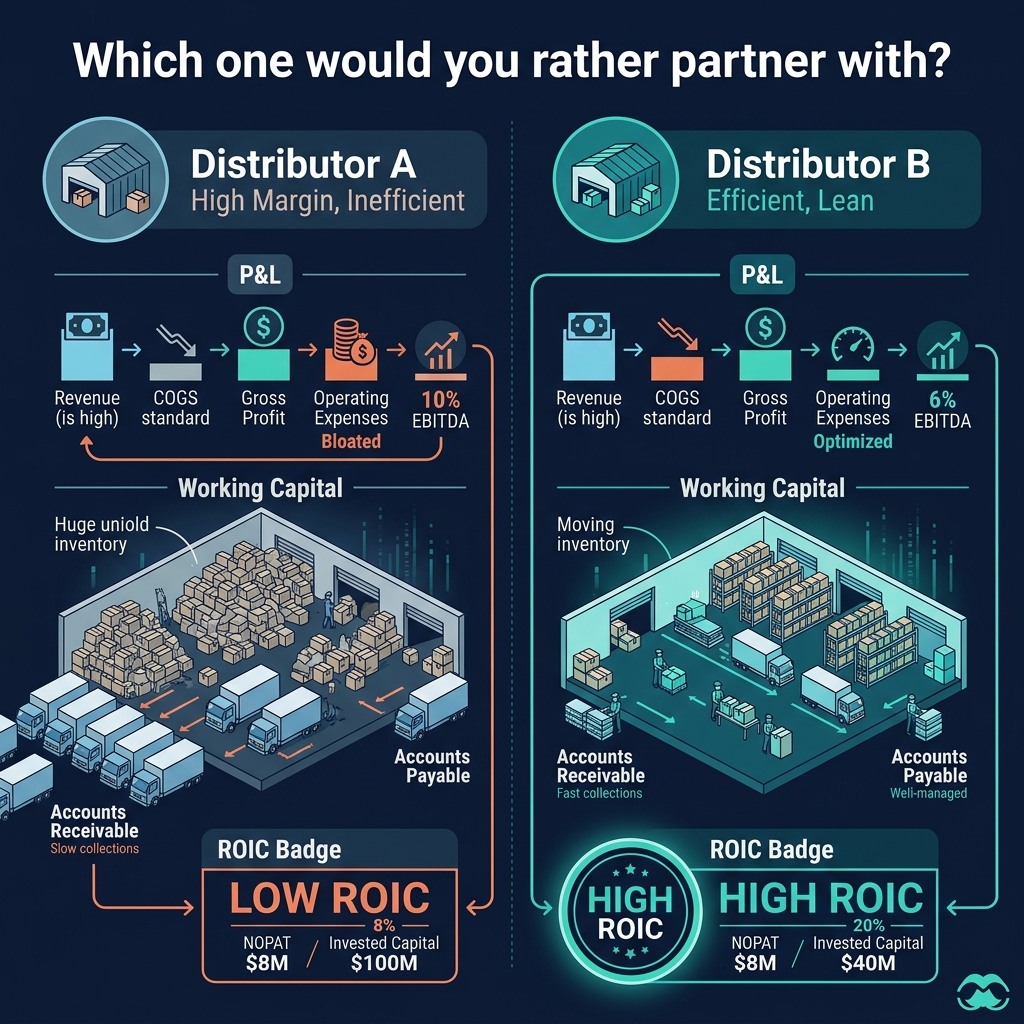

Once you accept that working capital is dominant, the distributor P&L looks different. The EBITDA margin - the headline number most P&Ls lead with - is still relevant. But the more important number is return on invested capital (ROIC), which measures the EBITDA against the capital tied up in the business, dominated by working capital. A distributor with a 6% EBITDA margin and efficient working capital can easily outperform a distributor with a 10% margin and bloated working capital. The first is a better business to partner with.

The ROIC calculation also surfaces the conversation about credit terms explicitly. Lowering the distributor's working capital through extended credit terms improves their ROIC directly, even holding EBITDA constant. The distributor sees it. The brand sees it. The conversation becomes "here's how the term sheet changes your economics" - quantified, visible, negotiable.

The platform's distributor audit flow enforces this framing. Working capital is a first-class input, not a footnote. The P&L renders ROIC alongside EBITDA as co-equal headline metrics. Credit terms are editable in the model, and the impact on both distributor ROIC and brand margin flows through instantly. A scenario that stresses credit terms can be modelled directly: "what if we extend terms from 30 to 45 days for the growth phase?"

The cultural shift

This reframing is a cultural shift, not just a modelling one. Brand teams trained to optimise DSO view longer credit terms as a concession. They're not wrong - longer terms do cost the brand something. But they're measuring the wrong thing. The question isn't "how do we minimise our cash exposure?" It's "how do we enable the distributor to execute the growth plan?" If the plan requires more working capital than the distributor can fund, and the brand can provide the cash via terms more cheaply than the distributor can borrow it externally, extending terms is the rational co-investment.

The platform's role is to make this visible. When the SP sits with the regional MD and the CFO to design the East Java deployment, the P&L shows the credit term impact explicitly. The CFO can see what the extension costs in brand DSO. The regional MD can see what it buys in distributor viability. The decision becomes a trade-off they can discuss, not a hidden subsidy nobody quantifies.

The broader point

Every commercial relationship has one or two constraints that dominate everything else. Naming them, surfacing them, and designing around them is most of the work. In distributor relationships, the constraint is working capital, and most platforms treat it as a line item when it should be the organising principle.

The same pattern applies in other domains. In supplier relationships, the dominant constraint is often payment cycles and quality assurance. In partnership relationships, it's often lead generation and attribution. In subscription businesses, it's often churn prevention and expansion. Identifying the dominant constraint and designing the platform's core conversation around it produces a different product than building a generic relationship manager.

Vertical platforms get this right by domain immersion. You can't identify the dominant constraint without spending enough time in the industry to see which variables actually move the business. Spreadsheet-literate analysts can see that working capital is a big number. Only commercial practitioners can see that working capital is the conversation. The platform's job is to turn the practitioner's insight into a first-class feature that shapes how users think and act.